The Reserve Bank of India on June 18, 2021, announced that it has given an ‘in-principle’ nod to Centrum Financial Services to set up a small finance bank (SFB).

This “in-principle” approval has been accorded in specific pursuance to the Centrum Financial Services Limited’s offer dated February 1, 2021, in response to the Expression of Interest notification dated November 3, 2020.

Objectives of the RBI initiative

The objectives of setting up of small finance banks are as follows:

(a) To further the aim of financial inclusion by providing an avenue of savings for the general masses

(b)To ensure the supply of credit for small business units, small and marginal farmers, micro and small industries; and other unorganized sector entities are maintained.

What are Small Finance Banks (SFBs)?

Small finance banks are a type of niche banks common in India. These small finance banks with the approved licenses can provide basic banking services such as acceptance of deposits and lending to those sections of the Indian economy not serviced by mainstream nationalized banks. These sections include small business units, small and marginal farmers, micro and small industries, and unorganized sector entities.

Small cooperative Banks continue to be under the rule of state governments through the registrar of

cooperative societies. This is where the local politicians are involved in a big way and laundering the

money collected from society members for personal benefits with or without the knowing of the political

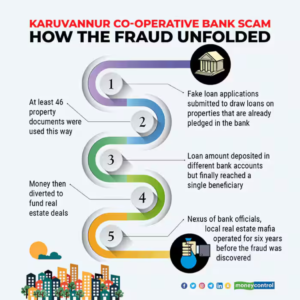

parties. The Karuvannur Cooperative bank scam shook up Kerala’s small banking industry at one point. The use of properties already pedged with bank shows that the banks officials were involved in the scam.

Another Karuvannur Bank-like scam is in the making, the Enforcement Directorate got the whiff, and informed the Kerala High Court last week. The probe agency has gathered information on similar fashion of money laundering through fake loan applications and financial irregularities through political nexus. The ED stated that the involvement of political parties, mainly politicians from the ruling Left, was found evident in the questioning of those linked to the case.

The development, involving at least 12 service co-operative banks, brings back the focus to a larger issue. In India, as per the current laws, only bigger cooperative banks come under the regulation of the Reserve Bank of India (RBI). Here, the regulator has been acting against the wrongdoers. So far in 2024 alone, there have been 20 instances of the RBI slapping monetary penalties on cooperative banks and revoking the licences of three.

Shree Mahalaxmi Mercantile Co-operative Bank, Hiriyur Urban Co-operative Bank, and Jai Prakash Narayan NagariSahakari Bank have lost their permits. The RBI actions, in most instances, came from weak capital ratios and poor corporate governance standards followed by the banks. The amount of monetary penalties imposed ranged from Rs 25,000 to Rs 3 lakh.

But, as far as smaller cooperative banks are concerned, there is no strong regulatory scrutiny yet. These small lenders continue to be under the rule of state governments through the registrar of cooperative societies, which throws open enough room for local politicians to play a role. The money collected from society members are often spent on personal benefits with or without the knowledge of the political parties. This needs to be stopped. I would like to make suggestions to avoid this situation.

Suggestions:

- Any person who is coming from political background should be prohibited to take any management post in Co-Operative Bank. If this is not possible, this type of banks should be under the continuous radar of RBI

- Nowadays, CBS is implemented in almost all Co Operative Banks. RBI and local registrar of cooperative societies should try to implement software which gives alert when advance is given on the basis of already pledged properties.

- The responsible officials who were found to be involved in the scam should be severely punished under criminal law. They should be removed from the job, and their retirement benefits should be forfeited.

- The real estate mafia or who was beneficiary of scam should be blacklisted to take any type of advance in future.

- Whenever finance is given on the basis of properties, its index or survey number should be input in the system and should be blocked as securities for further finance and RBI and Registrar should periodically check the controls.